Green Transition

Plug Power's $368.5M Cash Pile Still Outweighs Its Revenue Recovery

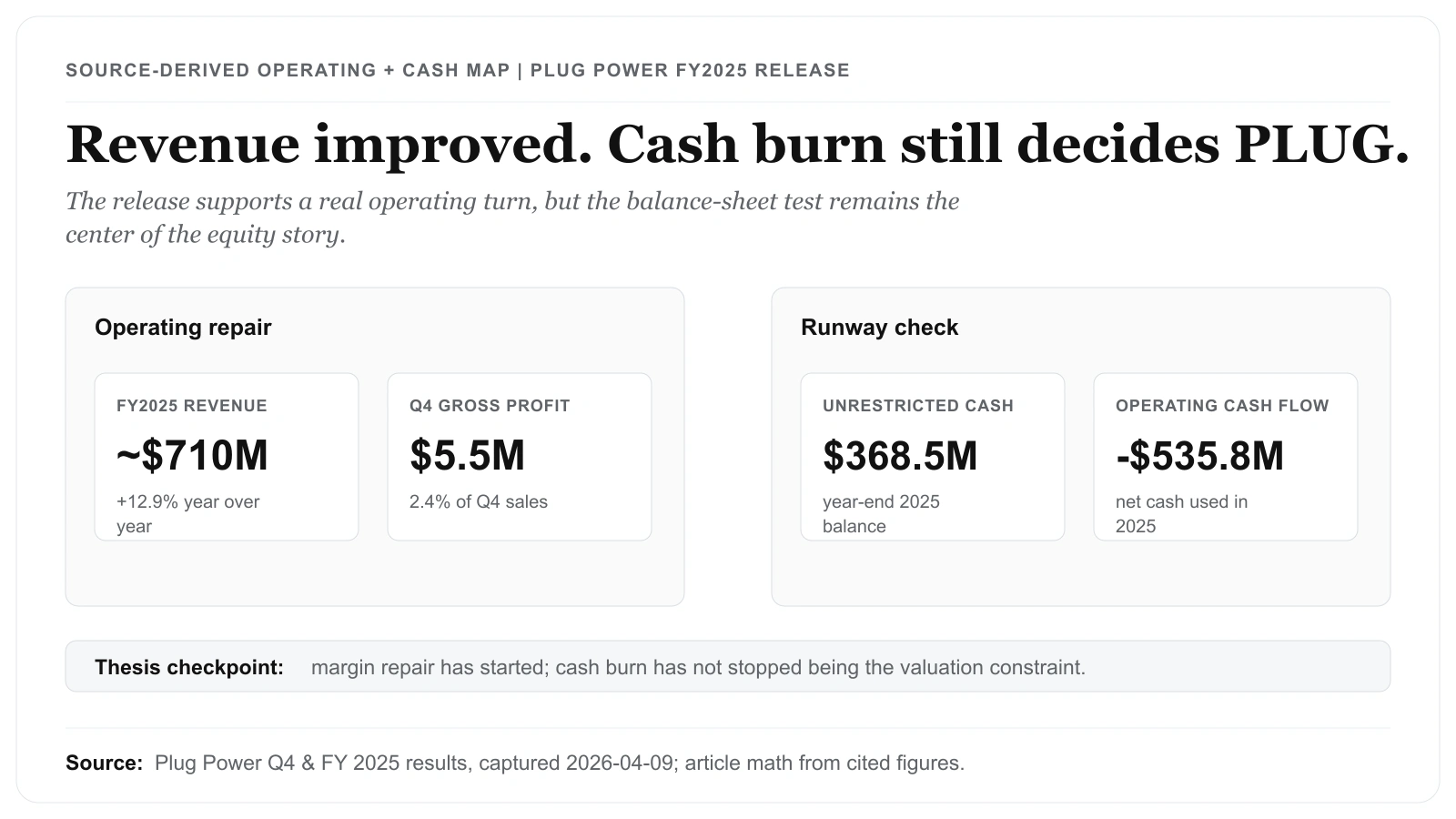

Plug Power's Q4 and full-year 2025 release showed 12.9% revenue growth to about $710 million, a return to positive quarterly gross profit, and $368.5 million of unrestricted cash. The 2026 issue is whether margin repair and asset monetization can reduce cash burn enough to extend the runway.

(Sources: Google Finance quote page for Plug Power, Plug Power Reports Q4 and Full Year 2025 Results with Strong Sales Growth and Margin Expansion)

The headline said turnaround: revenue up 12.9% to about $710 million, plus the first positive quarterly gross profit in a long stretch. The cash-flow statement said something harder. Net cash used in operating activities ran to $535.8 million for the year against $368.5 million of unrestricted cash at year-end — and once we set those two figures side by side, the margin-turnaround write-up this was supposed to be stopped holding together. The note below is built on the cash-flow statement and the asset-monetization figure instead, with the revenue headline as context rather than the frame.

Related reading: The KRBN Wrapper Is the First Check Before Carbon Credit Exposure | What the 2026 FOMC Calendar Says About When Fed Cuts Can Come | Verify Your Broker Before You Pick a Single U.S. Stock

Thesis

The immediate test for Plug Power is not a hydrogen-market size debate but whether the company has improved operations enough to keep its liquidity plan credible.

The official Q4 and full-year 2025 release gives a more concrete answer than the older hydrogen-economy narrative ever did. Plug Power said revenue increased 12.9% year over year to about $710 million in 2025, with fourth-quarter revenue of $225.2 million. It also reported $5.5 million of positive gross profit in Q4, equal to 2.4% of sales. Those are real operating improvements.

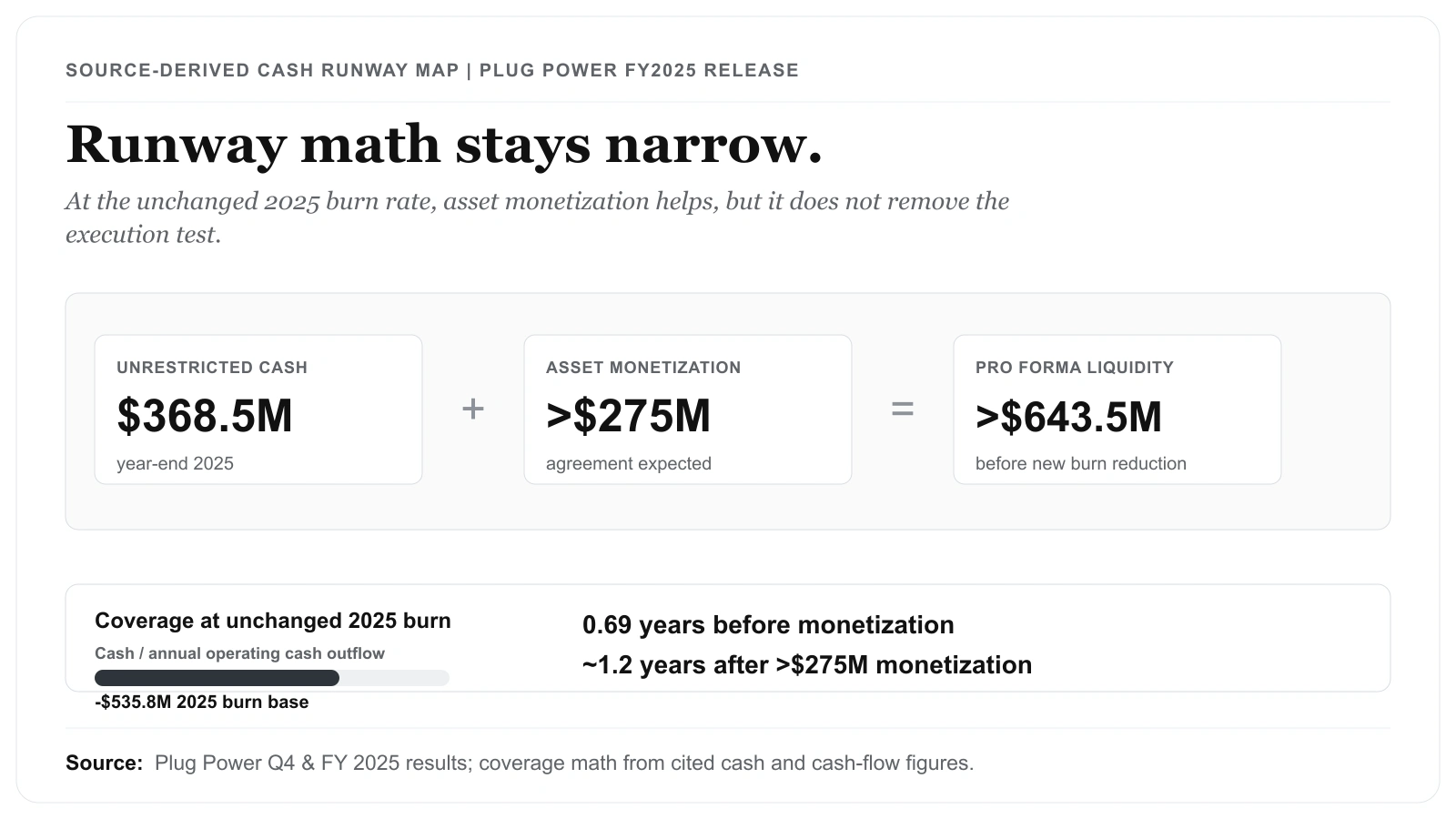

But the same release says unrestricted cash ended 2025 at $368.5 million, while net cash used in operating activities still totaled ($535.8 million) for the year. Plug also said an asset-monetization agreement is expected to generate more than $275 million. That is the full equity setup now: better revenue and margins, but still a balance-sheet case.

The positive case is that the worst margin damage is finally behind the company. The cautious case is that the cash-burn reduction still has to keep working quarter after quarter, not just on one earnings release.

Source Evidence Snapshot

The hero card now places Plug Power's operating repair beside the cash-burn test. The body evidence stack keeps the quote context and runway math as separate checks.

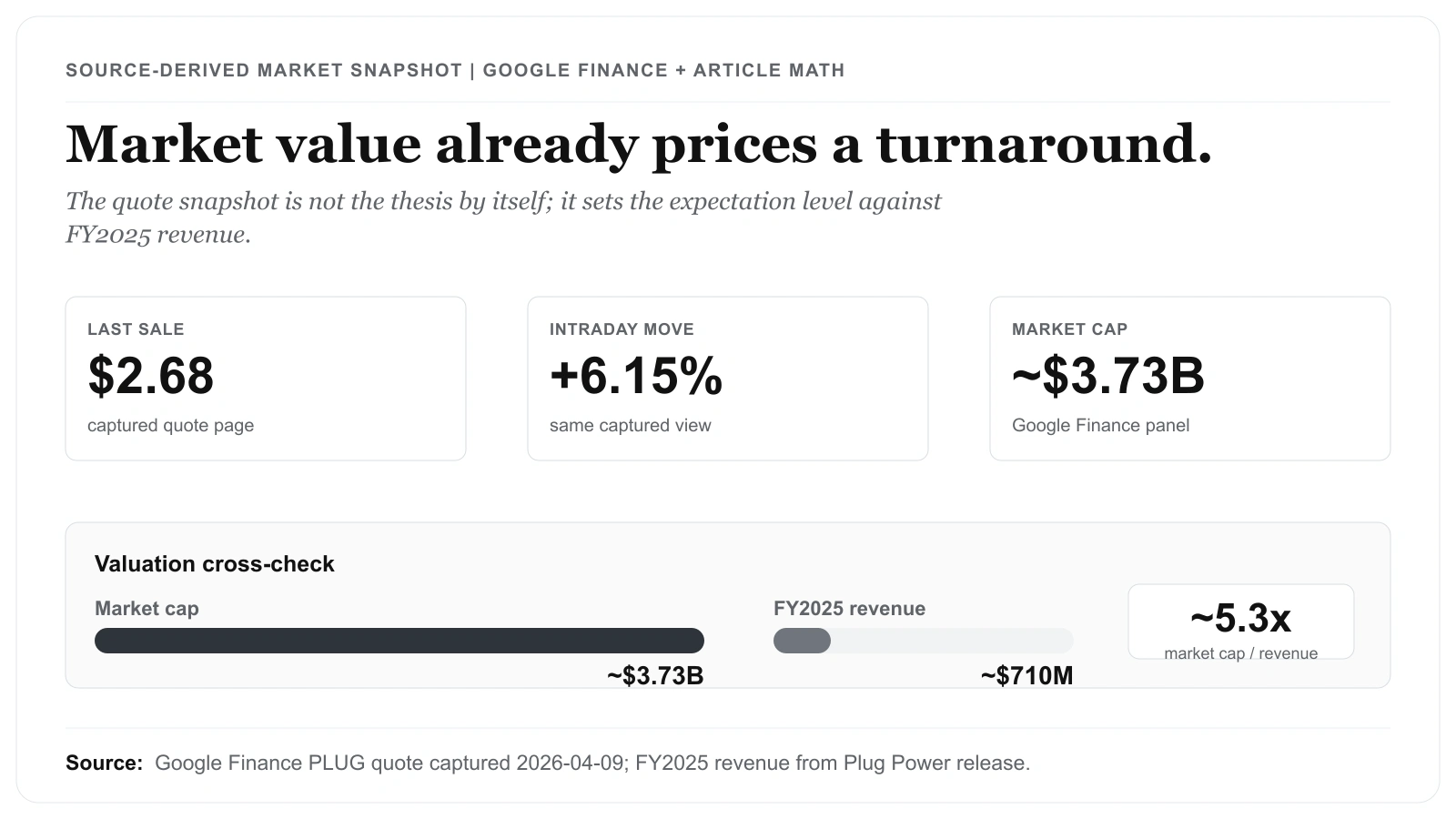

~5.3x cross-check are article math from market cap and revenue.The quote snapshot shows why expectations are still low. Plug traded at $2.68, up 6.15% on the day in the captured view, with a market cap of about $3.73 billion. For a company trying to finance a hydrogen buildout, that valuation means the market is still treating PLUG as a turnaround with real funding risk, not as a clean-energy company that has already settled the balance-sheet question.

The cash-flow statement is the reason the stock cannot be judged on headline revenue alone. Plug said net cash used in operating activities improved to ($535.8 million) in 2025 from ($728.6 million) in 2024. That is a real improvement, but it still leaves the company with a funding equation that depends on continued burn reduction and successful asset monetization.

What the Street is Pricing

Put the figures already in this post against each other and the setup sharpens. The market cap of about $3.73 billion against roughly $710 million of 2025 revenue is a price-to-sales multiple of about 5.3x. That is not the multiple of a forgotten balance-sheet casualty; it is a number that already prices in the revenue recovery and the asset-monetization story. The market is not ignoring Plug — it is paying ahead of proof.

The runway math is the harder read. Unrestricted cash of $368.5 million against full-year operating cash outflow of $535.8 million is roughly 0.69 years of coverage — about eight months at the unchanged 2025 burn rate. Fold in the $275+ million asset-monetization agreement and pro-forma liquidity of about $643.5 million covers roughly 1.2 years at that same rate. So the entire equity case sits in a narrow band: the 5.3x sales multiple is already underwriting a burn trajectory that today buys only about a year even after monetization.

That is why the public-market setup is binary around execution, not direction. If margin repair drives the burn rate below the 2025 level, that one-year coverage window stretches and the 5.3x multiple starts to look earned. If cash use holds near $535.8 million, the revenue recovery cannot carry a sales multiple that is already priced for the turnaround to work.

Revenue and Margin Repair Finally Moved in the Right Direction

The strongest part of the quarter is that Plug finally showed two things investors had been waiting to see together: higher revenue and positive quarterly gross profit.

Revenue of $225.2 million in Q4 and roughly $710 million for the year is not enough by itself to settle the hydrogen debate. What matters more is that Plug said positive Q4 gross profit reached $5.5 million, or 2.4% of sales, after a period when gross margins had been deeply negative.

That does not prove the turnaround is complete. It does show that better mix, pricing, fuel-network improvements, and service-cost reductions can change the direction of the business. The company explicitly tied the improvement to increased sales volume, favorable mix, increased pricing, and cost-per-unit reduction under Project Quantum Leap.

Plug also said electrolyzer revenue reached a record $187 million in 2025 and referenced an approximate $8 billion global sales funnel. Those lines matter because they suggest there is still a commercial business behind the hydrogen case, not just a capital-markets narrative.

Liquidity Is Better Framed, but It Is Not Comfortable Yet

Investors do not need to guess what the main bear point is. The company ended 2025 with $368.5 million of unrestricted cash, while full-year operating cash outflow remained ($535.8 million).

That is why the $275+ million asset-monetization agreement matters so much. Plug is effectively telling investors that operating improvement alone is not the only lever. It also needs liquidity transactions and reduced capex requirements to extend the runway.

The release frames this as a bridge to 2026. That may be fair. But the equity still reads like a balance-sheet-sensitive turnaround until multiple quarters show that the cash-burn trend is really improving, not just bouncing around on one report.

The Hydrogen Case Now Depends on Execution, Not Hype

The cleaner way to read Plug in 2026 is to stop asking whether hydrogen is exciting and start asking whether Plug can execute inside the parts of the market that are actually working.

The company highlighted engineering and project-planning milestones with Allied Green Ammonia, a 55-megawatt GenEco electrolyzer supply and service selection with Carlton Power across three UK projects, and an approximate 300 megawatts of GenEco electrolyzers deployed across four continents. Those are useful proof points because they show commercial traction beyond legacy optimism.

Still, none of those milestones erase the capital-intensity problem. Hydrogen infrastructure can become a real business and still be a difficult stock if the equity has to keep funding the gap before profits stabilize.

That is why PLUG still screens as a high-volatility turnaround rather than a clean compounder. The operating profile improved. The financing case still has to earn more trust.

Risks to the Thesis

The first risk is that positive Q4 gross profit does not persist. One profitable gross-profit quarter is useful evidence, but it does not yet prove that pricing, mix, fuel-network efficiency, and service-cost reductions will hold through a full demand cycle.

The second risk is liquidity execution. Asset monetization can extend the runway, but the stock still needs operating cash outflow to fall at the same time. If those two pieces diverge, the market can quickly return to dilution and refinancing concerns.

The third risk is project conversion. Electrolyzer milestones and ammonia or UK project references matter only if they become repeatable revenue with better working-capital behavior.

What Flips the Call

Three numbers matter more than the broader hydrogen narrative over the next few quarters.

First, watch whether gross profit stays positive and whether the margin line keeps moving away from the deeply negative levels of prior periods.

Second, watch unrestricted cash, asset-monetization proceeds, and operating cash outflow together. Plug does not need a perfect quarter. It does need the cash equation to keep improving in a visible way.

Third, watch whether electrolyzer and infrastructure projects convert into repeatable, cash-producing revenue rather than one-off milestones.

The latest release supports a more serious positive case than Plug had a year ago. It does not yet support a relaxed one. The numbers now justify watching PLUG as a real turnaround candidate, but they still do not justify forgetting that liquidity remains the center of the stock.