Market & Macro7 min read

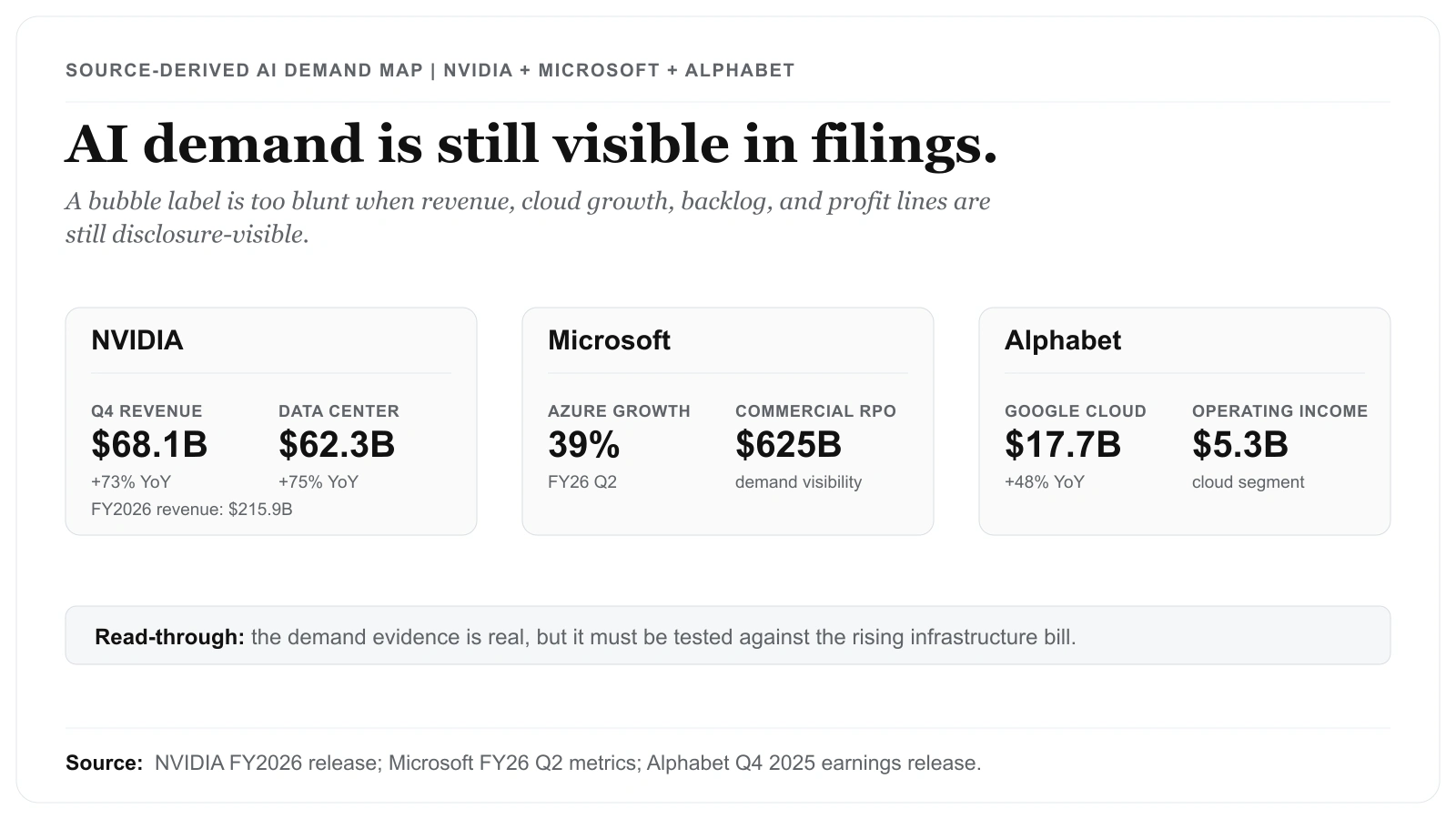

AI Stocks Still Show Real Revenue, but the CapEx Bar Has Risen

NVIDIA, Microsoft, and Alphabet disclosures, read side by side: which 2026 AI revenue is verified, and what the rising infrastructure bill actually costs.

Hynexly Research Team·